Navigating Roth IRA Contribution Limits for Married Couples in 2025

Navigating Roth IRA Contribution Limits for Married Couples in 2025

Introduction

In this auspicious occasion, we are delighted to delve into the intriguing topic related to Navigating Roth IRA Contribution Limits for Married Couples in 2025. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating Roth IRA Contribution Limits for Married Couples in 2025

The Roth IRA, a popular retirement savings vehicle, offers tax-free withdrawals in retirement, making it an attractive option for many Americans. However, understanding contribution limits is crucial for maximizing its benefits. For married couples filing jointly, these limits can be particularly relevant, as they allow for a combined savings potential.

While the exact contribution limits for 2025 are not yet finalized, projections based on historical trends and current economic conditions suggest that they will likely remain consistent with 2024 figures. This article will delve into the projected limits for married couples filing jointly, highlighting the importance of maximizing contributions and providing insights into the advantages of utilizing this retirement savings tool.

Projected Roth IRA Contribution Limits for Married Couples Filing Jointly in 2025

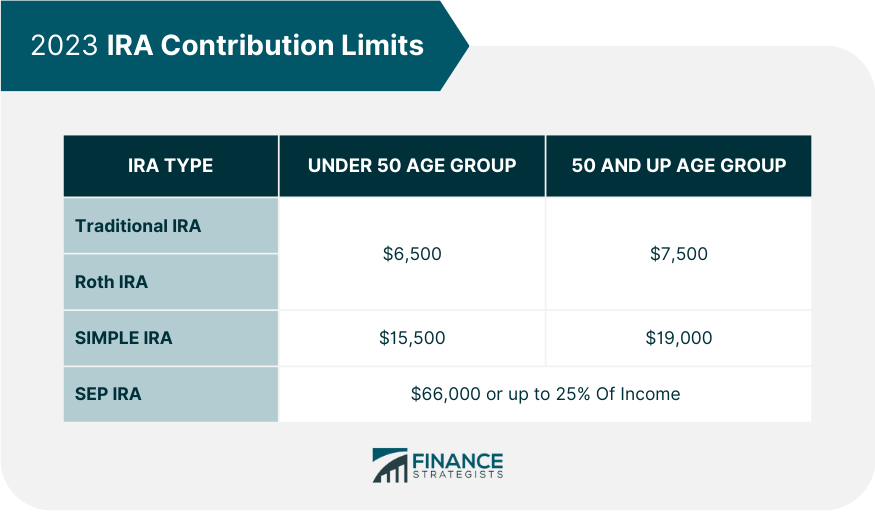

Based on current projections, the maximum contribution limit for a Roth IRA in 2025 is expected to be $7,500. This figure remains unchanged from 2024 and reflects the annual adjustment for inflation.

Understanding the Significance of Contribution Limits

The contribution limit represents the maximum amount an individual can contribute to their Roth IRA annually. For married couples filing jointly, each individual has their own separate Roth IRA account, allowing them to contribute up to the maximum limit, which effectively doubles their combined contribution potential.

Benefits of Maximizing Roth IRA Contributions

Maximizing contributions to a Roth IRA offers several advantages for married couples:

- Tax-Free Growth and Withdrawals: Contributions to a Roth IRA grow tax-free, and qualified withdrawals in retirement are also tax-free. This can significantly reduce the overall tax burden on retirement income.

- Flexibility and Control: Roth IRA contributions are made with after-tax dollars, allowing for greater flexibility in managing retirement savings. Individuals can choose to withdraw contributions at any time without penalty, providing access to funds if needed.

- Potential for Higher Returns: Early contributions to a Roth IRA have the potential to grow significantly over time due to compounding interest. The tax-free nature of withdrawals further enhances these returns.

- Income Eligibility: Unlike traditional IRAs, Roth IRA contributions are not subject to income restrictions. This makes it an accessible option for high-income earners who might not qualify for traditional IRA deductions.

Factors to Consider When Contributing to a Roth IRA

While maximizing contributions is generally beneficial, several factors should be considered when making Roth IRA contributions:

- Income Level: While there are no income restrictions for Roth IRA contributions, higher-income earners might consider other retirement savings options, such as 401(k) plans, due to potential income limitations on Roth IRA withdrawals.

- Financial Goals: Consider your overall financial goals and risk tolerance when deciding on Roth IRA contributions.

- Tax Bracket: If you anticipate being in a lower tax bracket in retirement, a Roth IRA might be a more advantageous option compared to a traditional IRA.

FAQs Regarding Roth IRA Contribution Limits for Married Couples Filing Jointly

Q: Can a married couple contribute to each other’s Roth IRAs?

A: No. Each individual must contribute to their own separate Roth IRA account.

Q: Can a married couple contribute to a Roth IRA even if one spouse is unemployed?

A: Yes. As long as the unemployed spouse meets the income eligibility requirements, they can contribute to a Roth IRA.

Q: What happens if I contribute more than the annual limit to my Roth IRA?

A: Excess contributions are subject to a 6% penalty. It’s essential to stay within the annual contribution limit to avoid penalties.

Q: Can I contribute to a Roth IRA and a traditional IRA simultaneously?

A: Yes. You can contribute to both a Roth IRA and a traditional IRA, but the total contributions across both accounts cannot exceed the annual limit.

Q: What happens to my Roth IRA contributions if I pass away?

A: Your Roth IRA will pass to your beneficiary according to your estate plan. Beneficiaries can withdraw the funds tax-free.

Tips for Maximizing Roth IRA Contributions

- Set a Budget: Allocate a specific amount of your income for Roth IRA contributions each month.

- Automate Contributions: Set up automatic transfers from your checking account to your Roth IRA to ensure regular contributions.

- Consider Catch-Up Contributions: If you are 50 or older, you can contribute an additional $1,000 annually, increasing your contribution limit to $8,500.

- Review Contributions Regularly: Adjust your contribution strategy as your income and financial goals change.

Conclusion

Understanding Roth IRA contribution limits for married couples filing jointly is crucial for maximizing retirement savings potential. By taking advantage of the combined contribution limit, couples can accumulate significant tax-free wealth for their future. While the exact limits for 2025 are still subject to change, staying informed about the current projections and implementing a strategic contribution plan can help couples achieve their financial goals and enjoy a comfortable retirement. Remember to consult with a financial advisor to determine the best retirement savings strategy for your individual circumstances.

+1000px.jpg)

Closure

Thus, we hope this article has provided valuable insights into Navigating Roth IRA Contribution Limits for Married Couples in 2025. We hope you find this article informative and beneficial. See you in our next article!