Navigating the 2025 Roth IRA Contribution Landscape for Individuals Over 50: A Comprehensive Guide

Navigating the 2025 Roth IRA Contribution Landscape for Individuals Over 50: A Comprehensive Guide

Introduction

With enthusiasm, let’s navigate through the intriguing topic related to Navigating the 2025 Roth IRA Contribution Landscape for Individuals Over 50: A Comprehensive Guide. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating the 2025 Roth IRA Contribution Landscape for Individuals Over 50: A Comprehensive Guide

The Roth IRA offers a valuable avenue for retirement savings, particularly for those over 50 who seek tax-free withdrawals in retirement. Understanding the contribution limits, especially the "catch-up" provision for those over 50, is crucial for maximizing retirement savings potential. This article delves into the 2025 Roth IRA contribution limits for individuals over 50, providing clarity and insights into this important aspect of retirement planning.

Understanding the 2025 Contribution Limits

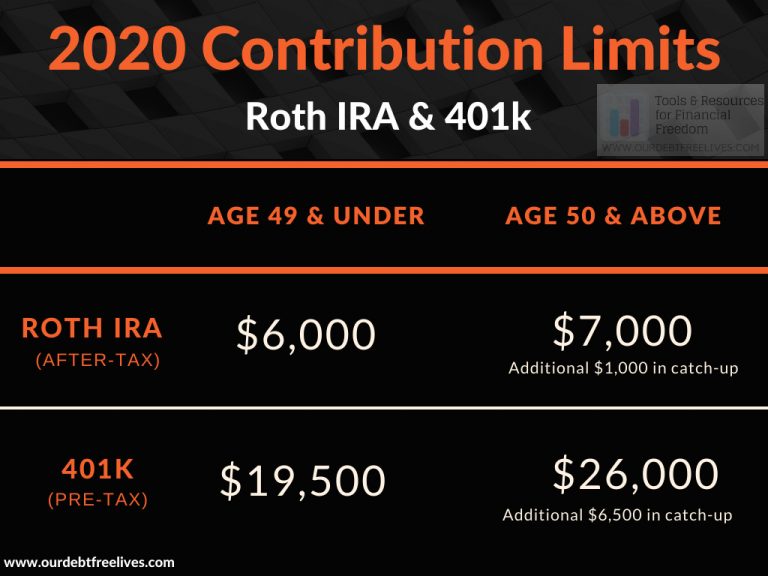

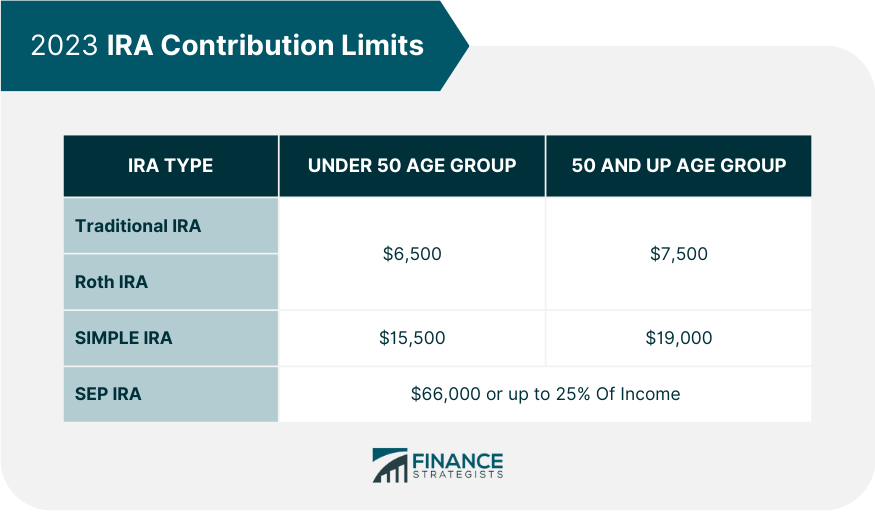

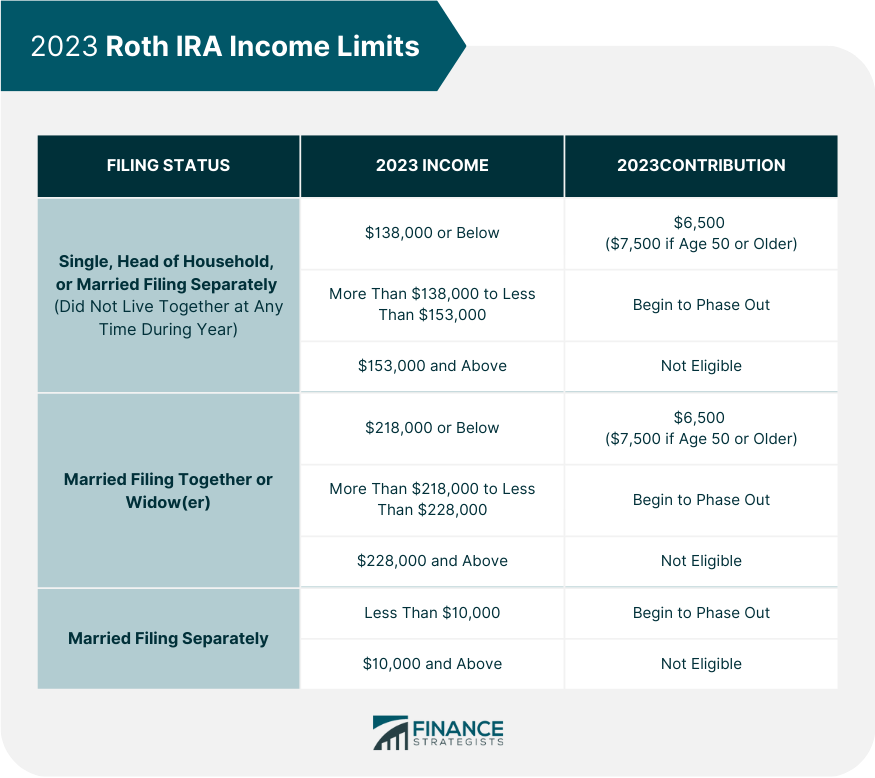

The Internal Revenue Service (IRS) sets annual contribution limits for Roth IRAs. For 2025, the general contribution limit for individuals of all ages is expected to remain at $6,500. However, individuals aged 50 and older benefit from a "catch-up" provision, allowing them to contribute an additional $1,000 annually. This means that in 2025, individuals over 50 can contribute up to $7,500 to their Roth IRA.

Why the Catch-Up Contribution Matters

The catch-up contribution is a valuable tool for individuals over 50, allowing them to accelerate their retirement savings. It provides an opportunity to compensate for lost time and potentially bridge the gap between their current savings and their retirement goals.

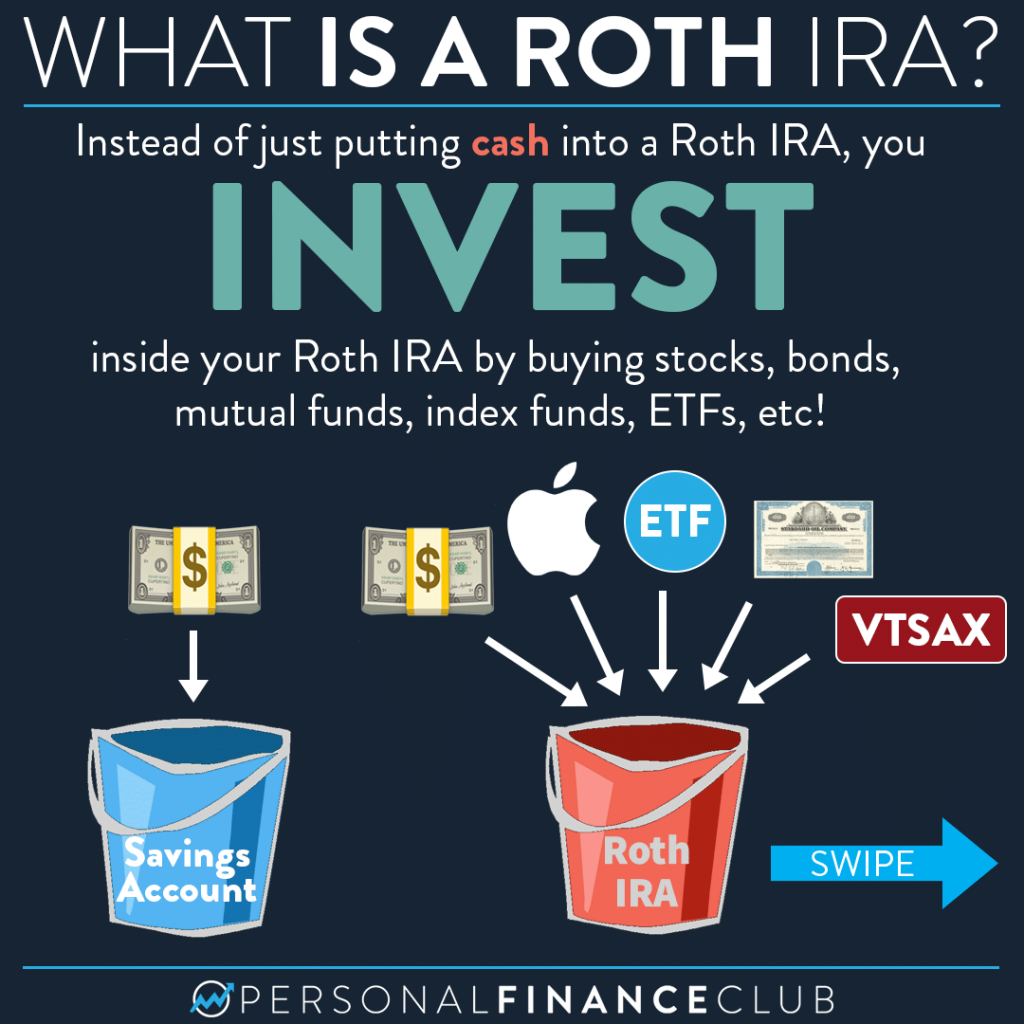

Benefits of a Roth IRA

Contributing to a Roth IRA offers several advantages, especially for those over 50:

- Tax-Free Withdrawals in Retirement: The primary benefit of a Roth IRA is that qualified withdrawals in retirement are tax-free. This means you will not have to pay taxes on your earnings or withdrawals in retirement.

- Potential for Tax-Free Growth: Your contributions and earnings grow tax-deferred within the Roth IRA. This tax-free growth can significantly enhance your retirement savings over time.

- Flexibility: Roth IRAs offer flexibility in terms of withdrawals. You can withdraw your contributions at any time, tax-free and penalty-free. However, withdrawals of earnings before age 59 1/2 are generally subject to taxes and penalties.

- No Required Minimum Distributions (RMDs): Unlike traditional IRAs, Roth IRAs do not have RMDs. This means you are not required to start taking withdrawals at a certain age, allowing your savings to continue growing tax-free.

Factors to Consider When Contributing to a Roth IRA

While the Roth IRA offers numerous benefits, it’s important to consider certain factors before making a contribution:

- Income Limits: There are income limits for contributing to a Roth IRA. If your modified adjusted gross income exceeds a certain threshold, you may not be able to contribute to a Roth IRA or your contributions may be phased out. For 2025, these limits are expected to remain at $153,000 for single filers and $228,000 for married couples filing jointly.

- Retirement Goals: Assess your retirement goals and savings needs. Consider your current savings, expected expenses, and desired retirement lifestyle.

- Other Retirement Accounts: Evaluate your existing retirement accounts, such as 401(k)s and traditional IRAs, and their respective contribution limits and tax implications.

- Tax Bracket: Consider your current and projected tax bracket. If you expect to be in a higher tax bracket in retirement, a Roth IRA may be a more advantageous option.

FAQs

Q: Can I contribute to both a traditional IRA and a Roth IRA in 2025?

A: Yes, you can contribute to both a traditional IRA and a Roth IRA in 2025. However, the total contributions to both types of IRAs cannot exceed the annual contribution limit. For 2025, this limit is expected to be $6,500 for individuals under 50 and $7,500 for individuals 50 and over.

Q: Can I contribute to a Roth IRA if I already have a 401(k)?

A: Yes, you can contribute to a Roth IRA even if you have a 401(k). However, your combined contributions to both types of accounts cannot exceed the annual contribution limit.

Q: What happens if I exceed the Roth IRA contribution limit?

A: If you exceed the Roth IRA contribution limit, the IRS will assess a 6% penalty on the excess contribution. You may also be required to pay taxes on the excess contribution.

Q: Can I withdraw my Roth IRA contributions before age 59 1/2?

A: You can withdraw your Roth IRA contributions at any time, tax-free and penalty-free. However, withdrawals of earnings before age 59 1/2 are generally subject to taxes and penalties.

Q: What happens to my Roth IRA if I pass away?

A: Your Roth IRA will pass to your beneficiaries according to your will or estate plan. Your beneficiaries will generally inherit the Roth IRA and can continue to grow the funds tax-deferred.

Tips for Maximizing Your Roth IRA Contributions

- Contribute Early and Often: Start contributing to your Roth IRA as early as possible to benefit from the power of compound growth.

- Maximize Your Catch-Up Contributions: If you are over 50, take full advantage of the catch-up contribution to accelerate your retirement savings.

- Consider Automatic Contributions: Set up automatic contributions from your paycheck to ensure you are consistently saving for retirement.

- Invest Wisely: Choose investments that align with your risk tolerance and time horizon. Consider a diversified portfolio of stocks, bonds, and other assets.

- Review Your Contributions Regularly: Periodically review your Roth IRA contributions and investment strategy to ensure it aligns with your evolving financial goals.

Conclusion

The Roth IRA, particularly with the catch-up provision for individuals over 50, presents a powerful tool for retirement savings. By understanding the contribution limits, benefits, and considerations, individuals can effectively utilize this vehicle to secure their financial future. Remember, the earlier you start contributing and the more you contribute, the greater the potential for tax-free growth and a comfortable retirement. Consult with a financial advisor to develop a personalized retirement savings strategy that best suits your needs and circumstances.

Closure

Thus, we hope this article has provided valuable insights into Navigating the 2025 Roth IRA Contribution Landscape for Individuals Over 50: A Comprehensive Guide. We hope you find this article informative and beneficial. See you in our next article!