Navigating Retirement Savings in 2025: A Comprehensive Guide to IRA Contribution Limits

Navigating Retirement Savings in 2025: A Comprehensive Guide to IRA Contribution Limits

Introduction

In this auspicious occasion, we are delighted to delve into the intriguing topic related to Navigating Retirement Savings in 2025: A Comprehensive Guide to IRA Contribution Limits. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating Retirement Savings in 2025: A Comprehensive Guide to IRA Contribution Limits

The journey to retirement is a long one, requiring careful planning and consistent contributions to ensure financial security. One of the most powerful tools available to individuals is the Individual Retirement Account (IRA), a tax-advantaged savings vehicle designed specifically for retirement planning. Understanding the nuances of IRA contribution limits is crucial for maximizing savings potential and achieving desired retirement outcomes.

IRA Contribution Limits: A Framework for Retirement Savings

The Internal Revenue Service (IRS) sets annual contribution limits for IRAs, which can vary based on age and participation in other retirement plans. These limits are designed to promote equitable access to retirement savings while ensuring the long-term sustainability of the program.

2025 IRA Contribution Limits: A Snapshot

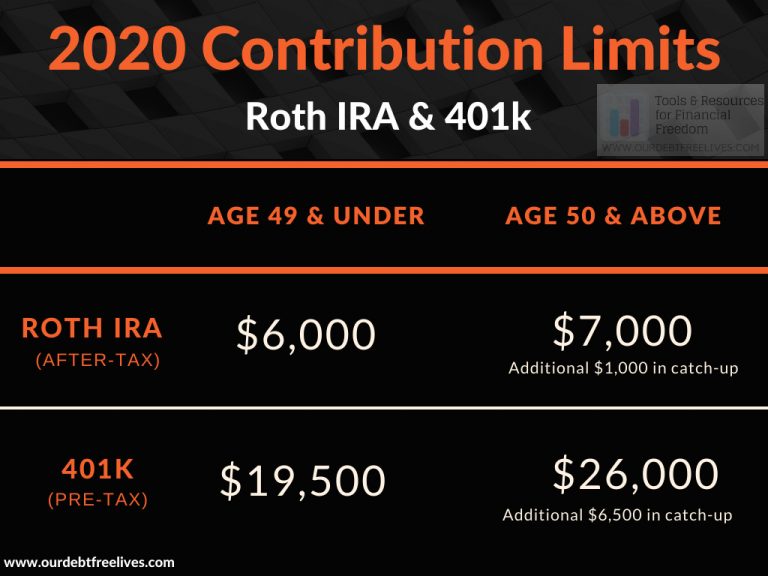

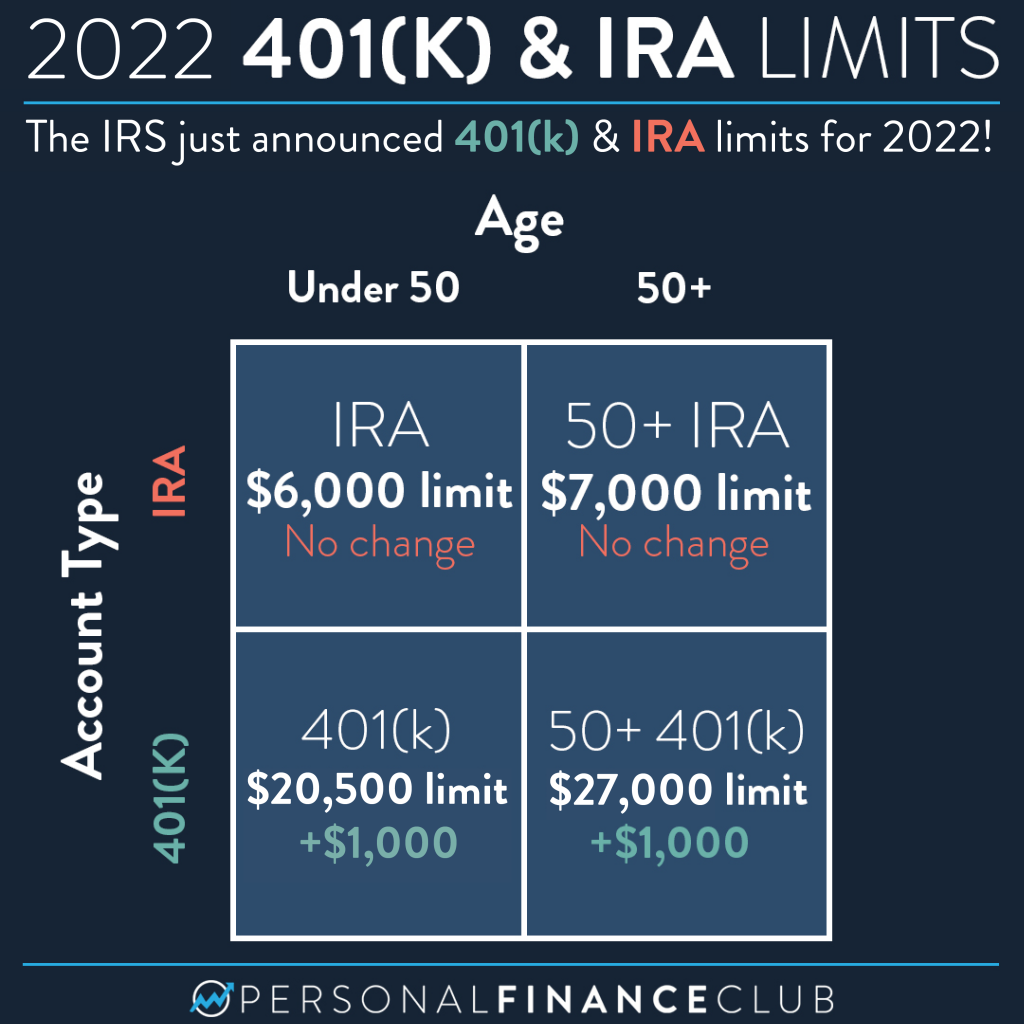

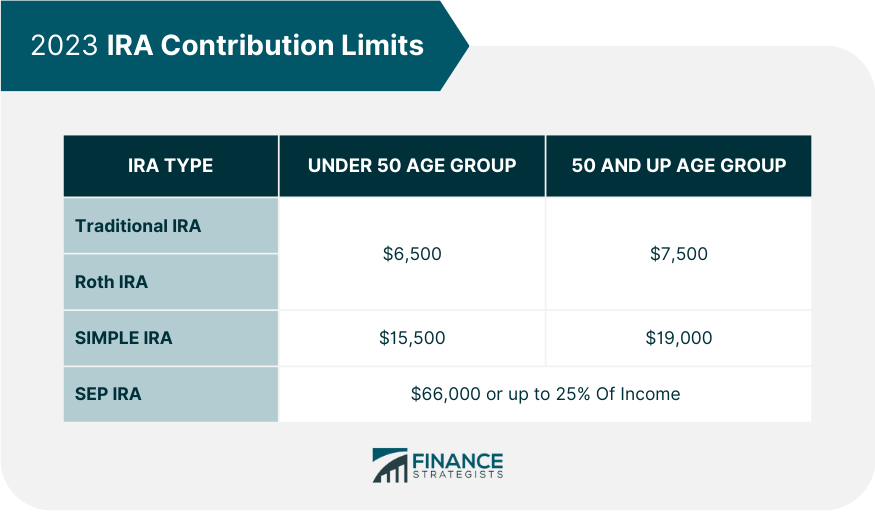

As of 2025, the maximum annual contribution to a traditional or Roth IRA for individuals under age 50 is $6,500. This amount is subject to change based on annual IRS adjustments for inflation. Individuals aged 50 and over can contribute an additional $1,000 per year, known as the "catch-up contribution." This brings the total maximum contribution for those 50 and older to $7,500.

Understanding the Significance of IRA Contribution Limits

The IRA contribution limits play a critical role in retirement planning, acting as a guideline for maximizing tax advantages and building a substantial nest egg. By adhering to these limits, individuals can:

- Maximize tax benefits: Traditional IRAs allow pre-tax contributions, reducing taxable income in the present. Roth IRAs, on the other hand, offer tax-free withdrawals in retirement.

- Compound growth: The power of compounding works most effectively with consistent contributions over time. Maximum contributions ensure the full potential of compound growth is realized.

- Retirement security: By contributing the maximum allowed, individuals can build a substantial retirement nest egg, providing financial security in later years.

Delving Deeper: The Impact of Age and Other Factors

While the contribution limits are straightforward, understanding their application to different scenarios is crucial. Here’s a breakdown of key factors impacting IRA contributions:

- Age: The catch-up contribution for individuals 50 and older provides an opportunity to accelerate savings in the years leading up to retirement. This additional contribution can significantly enhance retirement income.

- Other Retirement Plans: Individuals participating in employer-sponsored retirement plans, such as 401(k)s, may have modified IRA contribution limits. The IRS provides specific rules and guidance for these scenarios.

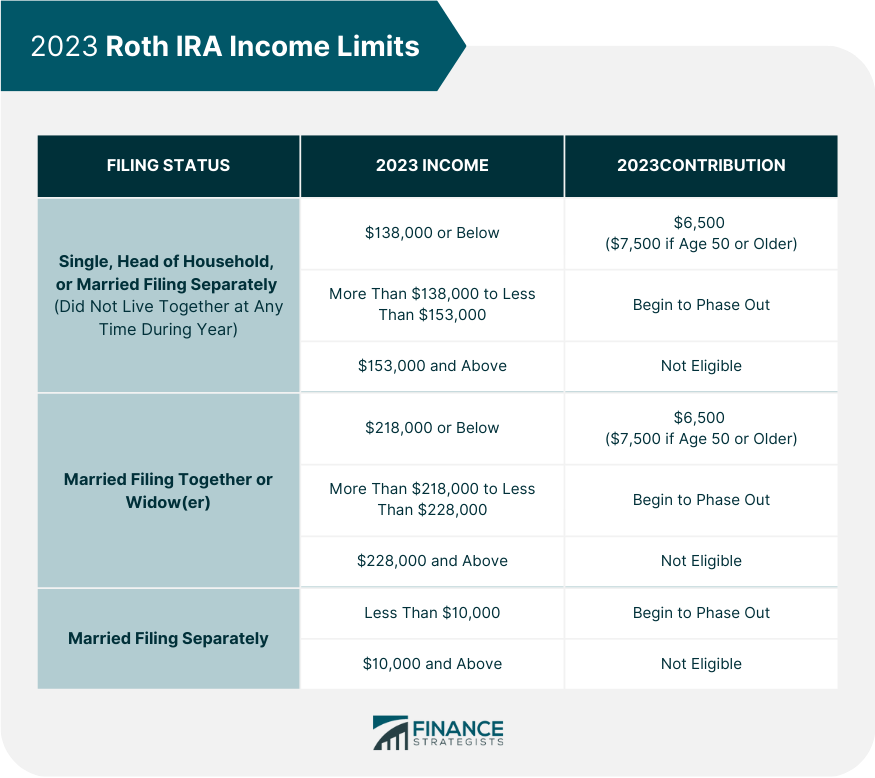

- Modified Adjusted Gross Income (MAGI): Roth IRA contributions are subject to income limitations. Individuals with MAGIs exceeding certain thresholds may be restricted or completely prohibited from contributing to a Roth IRA.

Navigating IRA Contributions: A Practical Guide

With the intricacies of contribution limits in mind, it’s essential to approach IRA contributions strategically. Here are some key considerations:

- Contribution Strategy: Develop a personalized savings plan that considers your financial goals, risk tolerance, and time horizon.

- Contribution Timing: Maximize tax benefits by contributing early in the year, allowing for potential tax savings.

- Contribution Frequency: Regular contributions, even in small amounts, can significantly impact long-term savings.

- Professional Guidance: Seek advice from a qualified financial advisor to ensure your contributions align with your overall financial plan.

FAQs: Addressing Common Questions about IRA Contribution Limits

Q: Can I contribute to both a traditional and Roth IRA in the same year?

A: Yes, individuals can contribute to both a traditional and Roth IRA in the same year, up to the annual maximum contribution limit for each account. However, income limitations may apply to Roth IRA contributions.

Q: What happens if I contribute more than the annual limit?

A: Exceeding the annual contribution limit may result in penalties. It’s crucial to carefully track contributions and avoid over-contributing.

Q: Can I withdraw contributions from my IRA before retirement?

A: Withdrawals from traditional IRAs are generally subject to taxes and potentially penalties. Roth IRA withdrawals before age 59 1/2 are tax-free and penalty-free if they meet specific criteria.

Q: What are the tax implications of IRA contributions?

A: Traditional IRA contributions are tax-deductible, reducing taxable income. Roth IRA contributions are made with after-tax dollars, but withdrawals in retirement are tax-free.

Q: How do I choose between a traditional and Roth IRA?

A: The choice between a traditional and Roth IRA depends on individual circumstances, including income level, expected tax bracket in retirement, and anticipated future tax rates. Consulting with a financial advisor can help determine the best option for your situation.

Conclusion: A Foundation for a Secure Retirement

Understanding and effectively utilizing IRA contribution limits is a cornerstone of successful retirement planning. By maximizing contributions, individuals can take advantage of tax benefits, leverage the power of compound growth, and build a substantial nest egg to ensure financial security in their golden years. Regular review and adjustment of contribution strategies, alongside professional guidance, can ensure a smooth and fulfilling transition into retirement.

Closure

Thus, we hope this article has provided valuable insights into Navigating Retirement Savings in 2025: A Comprehensive Guide to IRA Contribution Limits. We appreciate your attention to our article. See you in our next article!