A Guide to SEP IRA Contributions in 2025 for Individuals Over 50

A Guide to SEP IRA Contributions in 2025 for Individuals Over 50

Introduction

With enthusiasm, let’s navigate through the intriguing topic related to A Guide to SEP IRA Contributions in 2025 for Individuals Over 50. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

A Guide to SEP IRA Contributions in 2025 for Individuals Over 50

:max_bytes(150000):strip_icc()/sep.asp-final-a70730c1f5034f9780d458bee74059b1.jpg)

The Simplified Employee Pension (SEP) IRA is a retirement savings plan designed for self-employed individuals and small business owners. It offers significant tax advantages and flexibility, making it a valuable tool for those seeking to secure their financial future. This article explores the intricacies of SEP IRA contributions in 2025 for individuals over 50, emphasizing the unique benefits and considerations that come with this age group.

Understanding the SEP IRA Contribution Limits

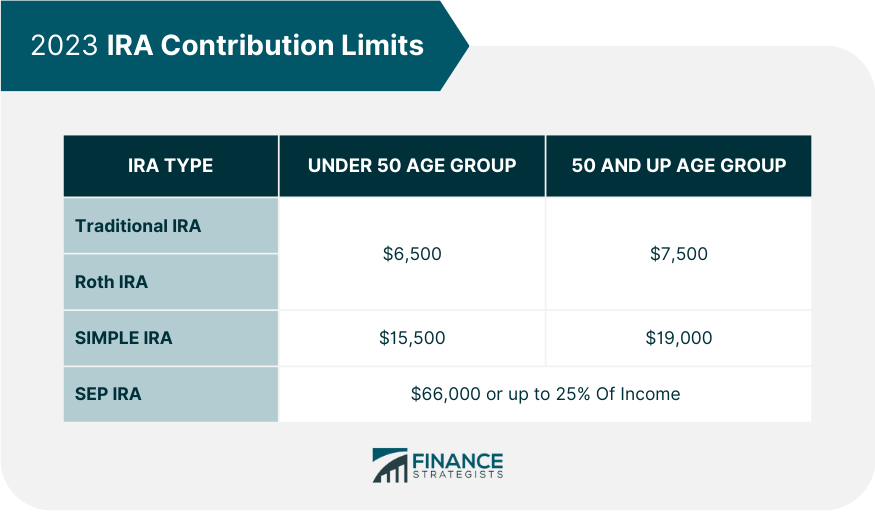

The contribution limit for SEP IRAs in 2025 is subject to annual adjustments based on inflation. The Internal Revenue Service (IRS) typically announces these adjustments in late fall or early winter of the preceding year. While the exact limit for 2025 is not yet known, it is expected to be similar to or slightly higher than the 2024 limit.

For 2024, the maximum contribution is 25% of your net adjusted self-employed income or $66,000, whichever is less. This means that if your net adjusted self-employed income is $200,000 in 2024, you can contribute a maximum of $50,000 (25% of $200,000) to your SEP IRA.

Catch-Up Contributions for Individuals Over 50

One of the most attractive features of SEP IRAs for individuals over 50 is the availability of catch-up contributions. This allows individuals to contribute an additional amount beyond the regular contribution limit to make up for lost savings opportunities.

For 2024, individuals aged 50 and older can contribute an extra $1,000 on top of the regular contribution limit, bringing the total maximum contribution to $67,000. This extra contribution amount is subject to annual adjustments, similar to the regular contribution limit.

Benefits of SEP IRA Contributions for Individuals Over 50

-

Tax Advantages: SEP IRA contributions are tax-deductible, meaning they reduce your taxable income, resulting in immediate tax savings. Additionally, your investment earnings grow tax-deferred, meaning you won’t be taxed on them until you withdraw the funds in retirement.

-

Flexibility: SEP IRAs offer flexibility in contribution amounts. You can choose to contribute the maximum amount allowed each year or contribute a lesser amount based on your financial situation. This flexibility allows you to tailor your retirement savings strategy to your individual needs.

-

Catch-Up Contributions: The availability of catch-up contributions allows individuals over 50 to accelerate their retirement savings and potentially offset any lost saving opportunities during their earlier working years.

-

Simplicity: SEP IRAs are relatively simple to set up and manage compared to other retirement plans.

Considerations for SEP IRA Contributions Over 50

-

Income Limit: The contribution limit for SEP IRAs is tied to your net adjusted self-employed income. This means that if your income is low, your maximum contribution will be limited accordingly.

-

Withdrawal Penalties: While SEP IRA withdrawals are tax-free after age 59 1/2, early withdrawals before that age are subject to a 10% penalty, in addition to regular income taxes.

-

Investment Choices: The investment options available within a SEP IRA may be limited compared to other retirement plans.

FAQs about SEP IRA Contributions in 2025 for Individuals Over 50

Q: When will the 2025 SEP IRA contribution limits be announced?

A: The IRS typically announces the contribution limits for the following year in late fall or early winter of the preceding year.

Q: Can I contribute to a SEP IRA even if I have a 401(k) or other retirement plan?

A: Yes, you can contribute to a SEP IRA even if you participate in other retirement plans. However, there are limits on the total amount you can contribute across all plans.

Q: How do I calculate my net adjusted self-employed income for SEP IRA contributions?

A: Your net adjusted self-employed income is calculated by subtracting your business expenses from your self-employment income. Consult with a tax professional for detailed guidance on calculating this figure.

Q: Are there any age restrictions for contributing to a SEP IRA?

A: There are no age restrictions for contributing to a SEP IRA. However, individuals over 50 can take advantage of catch-up contributions.

Q: Can I withdraw contributions from my SEP IRA before age 59 1/2?

A: You can withdraw contributions from your SEP IRA before age 59 1/2 without penalty. However, you will be subject to regular income taxes on the withdrawal.

Q: Can I roll over assets from another retirement account into a SEP IRA?

A: Yes, you can roll over assets from other retirement accounts, such as 401(k)s, traditional IRAs, or Roth IRAs, into a SEP IRA.

Tips for Maximizing SEP IRA Contributions in 2025 for Individuals Over 50

-

Contribute Early and Often: The sooner you start contributing to your SEP IRA, the more time your investments have to grow tax-deferred.

-

Take Advantage of Catch-Up Contributions: If you are over 50, maximize your retirement savings by taking advantage of the catch-up contribution limit.

-

Consider a Roth SEP IRA: A Roth SEP IRA allows you to contribute after-tax dollars, but your withdrawals in retirement are tax-free.

-

Seek Professional Advice: Consult with a financial advisor or tax professional to determine the best SEP IRA strategy for your individual circumstances.

Conclusion

SEP IRAs offer a valuable retirement savings opportunity for self-employed individuals and small business owners. The availability of catch-up contributions for individuals over 50 further enhances the attractiveness of this plan, allowing for accelerated savings and a more secure financial future. By understanding the contribution limits, benefits, and considerations associated with SEP IRAs, individuals over 50 can effectively leverage this plan to build a robust retirement nest egg.

Closure

Thus, we hope this article has provided valuable insights into A Guide to SEP IRA Contributions in 2025 for Individuals Over 50. We appreciate your attention to our article. See you in our next article!