Navigating Retirement Savings in 2025: A Guide to IRA Contribution Limits for Individuals Under 50

Navigating Retirement Savings in 2025: A Guide to IRA Contribution Limits for Individuals Under 50

Introduction

With enthusiasm, let’s navigate through the intriguing topic related to Navigating Retirement Savings in 2025: A Guide to IRA Contribution Limits for Individuals Under 50. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating Retirement Savings in 2025: A Guide to IRA Contribution Limits for Individuals Under 50

The path to a secure retirement often involves strategic financial planning, and Individual Retirement Accounts (IRAs) play a crucial role in this endeavor. As of 2025, individuals under 50 have the opportunity to contribute a significant amount to their IRAs, maximizing their savings potential. Understanding the contribution limits and the benefits they offer is essential for making informed financial decisions.

Understanding IRA Contribution Limits

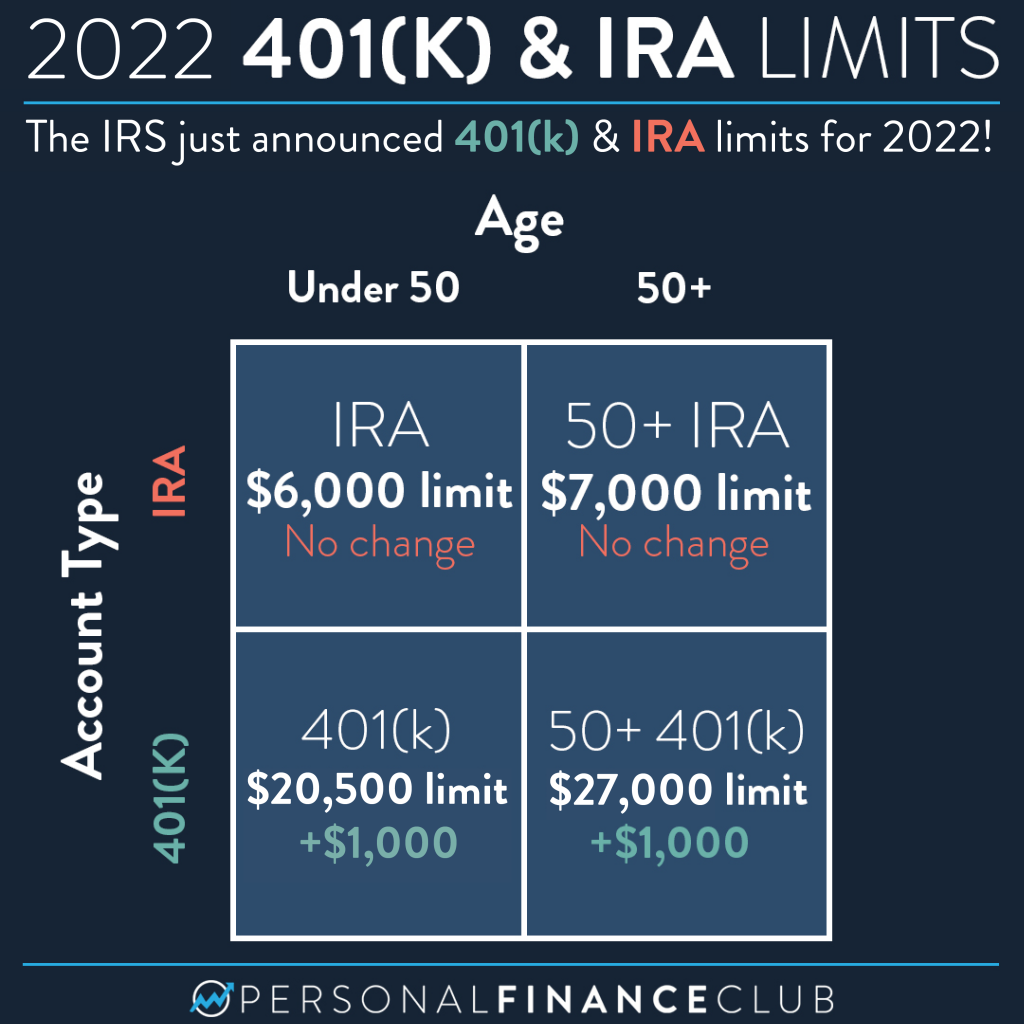

The annual contribution limit for traditional and Roth IRAs for individuals under 50 in 2025 is $6,500. This limit represents the maximum amount an individual can contribute to their IRA in a given year, regardless of their income level.

Why Are IRA Contribution Limits Important?

Contribution limits serve as a guideline for maximizing retirement savings. By understanding and adhering to these limits, individuals can:

- Maximize Tax Advantages: Traditional IRAs offer tax-deductible contributions, potentially reducing taxable income in the present. Roth IRAs, on the other hand, allow for tax-free withdrawals in retirement.

- Boost Retirement Savings: Contributing the maximum amount allowed each year can significantly accelerate the growth of retirement savings through compound interest.

- Enjoy Flexibility: IRAs offer flexibility in investment choices, allowing individuals to select a portfolio that aligns with their risk tolerance and financial goals.

- Prepare for the Future: Retirement planning is a long-term endeavor, and maximizing contributions early on can provide a solid foundation for financial security in later years.

Factors Influencing IRA Contribution Limits

While the annual contribution limit for individuals under 50 remains consistent, certain factors can influence the overall amount contributed:

- Income: For traditional IRAs, income limitations may apply, potentially reducing the deductible contribution amount.

- Age: Individuals aged 50 and above can contribute an additional "catch-up" amount to their IRA, increasing their annual contribution limit.

- Spousal IRA: If both spouses are eligible, they can each contribute the maximum amount to their respective IRAs.

Navigating IRA Contributions Effectively

To make the most of IRA contributions, individuals should consider:

- Contribution Timing: It is advisable to contribute early in the year to maximize the benefits of compound interest.

- Investment Strategy: Diversifying investments across different asset classes can help mitigate risk and enhance potential returns.

- Regular Reviews: Periodically reviewing investment performance and adjusting the portfolio as needed can help ensure alignment with financial goals.

- Seeking Professional Advice: Consulting with a financial advisor can provide personalized guidance on IRA contributions and investment strategies.

Frequently Asked Questions about IRA Contribution Limits in 2025

Q: Can I contribute more than $6,500 to my IRA in 2025 if I am under 50?

A: No, the maximum contribution limit for individuals under 50 in 2025 is $6,500. However, if you are 50 or older, you can contribute an additional "catch-up" amount of $1,000, increasing your total contribution limit to $7,500.

Q: What are the income limitations for contributing to a traditional IRA?

A: For 2025, if your Modified Adjusted Gross Income (MAGI) is $73,000 or higher as a single filer, or $146,000 or higher as a married couple filing jointly, your ability to deduct traditional IRA contributions may be limited or eliminated.

Q: Can I contribute to both a traditional IRA and a Roth IRA in 2025?

A: Yes, you can contribute to both a traditional IRA and a Roth IRA in 2025, but your total contributions cannot exceed $6,500.

Q: What happens if I contribute more than the maximum amount to my IRA?

A: Contributing more than the annual limit will result in penalties and taxes. It is crucial to stay within the contribution limits to avoid these financial consequences.

Tips for Maximizing IRA Contributions in 2025

- Automate Contributions: Setting up automatic contributions from your checking account can make saving consistently effortless.

- Consider a Roth IRA: If you expect to be in a higher tax bracket in retirement, a Roth IRA may be advantageous, as withdrawals are tax-free.

- Take Advantage of Employer Matching: If your employer offers a 401(k) plan with matching contributions, maximize those contributions to receive free money towards retirement.

- Don’t Forget About Catch-up Contributions: If you are 50 or older, consider contributing the additional "catch-up" amount to accelerate your retirement savings.

Conclusion

Understanding and utilizing the IRA contribution limits available in 2025 is a crucial step towards a secure financial future. By maximizing contributions, individuals can leverage the tax advantages and growth potential of IRAs to build a substantial retirement nest egg. Remember, retirement planning is a long-term endeavor, and starting early and contributing consistently can make a significant difference in achieving financial independence in later years. Seeking professional advice and staying informed about relevant regulations and limits can further enhance your retirement savings strategy.

:max_bytes(150000):strip_icc()/IRA_V1_4194258-7cf65db353ac41c48202e216dfbd46ee.jpg)

Closure

Thus, we hope this article has provided valuable insights into Navigating Retirement Savings in 2025: A Guide to IRA Contribution Limits for Individuals Under 50. We appreciate your attention to our article. See you in our next article!