Navigating Retirement Savings in 2025: Understanding the IRA Contribution Limits for Individuals Over 50

Navigating Retirement Savings in 2025: Understanding the IRA Contribution Limits for Individuals Over 50

Introduction

With great pleasure, we will explore the intriguing topic related to Navigating Retirement Savings in 2025: Understanding the IRA Contribution Limits for Individuals Over 50. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating Retirement Savings in 2025: Understanding the IRA Contribution Limits for Individuals Over 50

As individuals approach their golden years, securing financial stability becomes paramount. Retirement accounts, such as Individual Retirement Accounts (IRAs), play a crucial role in this endeavor, offering tax advantages and encouraging long-term savings. For those aged 50 and over, the Internal Revenue Service (IRS) provides an additional opportunity to bolster retirement savings through "catch-up contributions." This article aims to provide a comprehensive understanding of the IRA contribution limits for individuals over 50 in 2025, highlighting the benefits and considerations associated with this valuable financial tool.

Understanding the Basics: IRA Contribution Limits

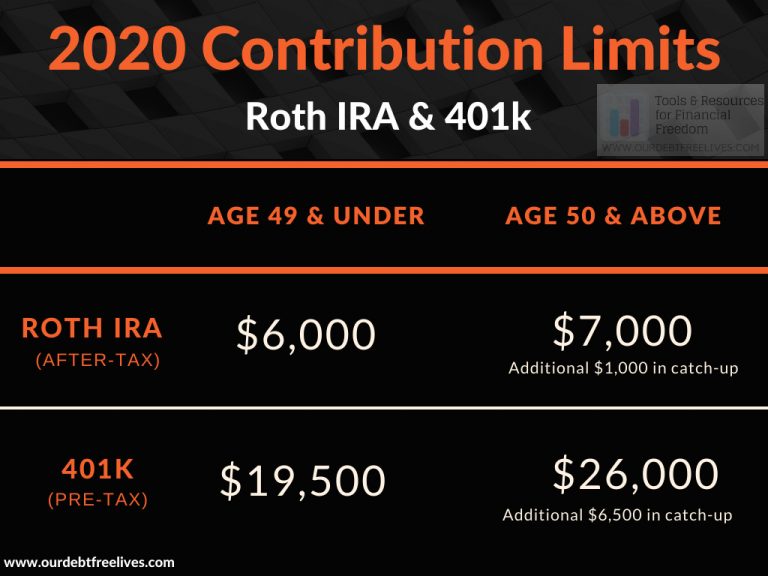

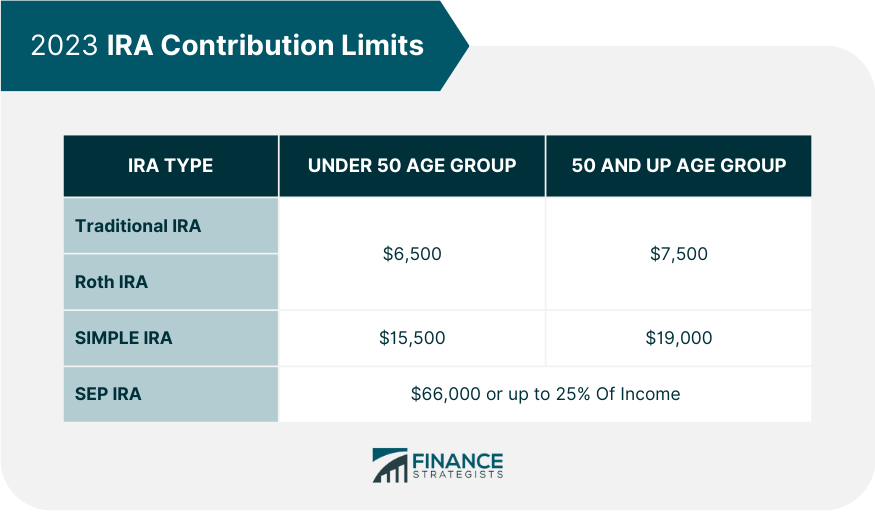

The IRS sets annual limits on contributions to both Traditional and Roth IRAs. These limits are designed to ensure fairness and encourage responsible saving. For 2023, the contribution limit for all individuals, regardless of age, is $6,500. However, individuals aged 50 and over are eligible for an additional "catch-up contribution" of $1,000, bringing their total annual contribution limit to $7,500.

While the 2025 contribution limits are yet to be officially announced, it is reasonable to anticipate a slight increase based on historical trends. The IRS typically adjusts contribution limits annually to account for inflation. It is crucial to stay informed about these adjustments as they are announced.

The Significance of Catch-Up Contributions

Catch-up contributions offer a unique opportunity for individuals over 50 to accelerate their retirement savings. This additional contribution allows for greater flexibility and potential for growth, especially in the later stages of one’s career. By taking advantage of these limits, individuals can bridge the gap between their desired retirement income and their accumulated savings.

Benefits of Utilizing Catch-Up Contributions

- Increased Retirement Savings: Catch-up contributions directly increase the total amount saved for retirement, potentially leading to a larger nest egg.

- Tax Advantages: Traditional IRAs offer tax-deductible contributions, reducing current tax liability. Roth IRAs provide tax-free withdrawals in retirement.

- Enhanced Financial Security: Higher retirement savings contribute to a greater sense of financial security and peace of mind during retirement.

- Potential for Compounding: The longer the savings are invested, the greater the potential for compound growth, allowing savings to grow exponentially over time.

Factors to Consider When Utilizing Catch-Up Contributions

- Income Limits: While there are no income limits for contributing to a Traditional IRA, Roth IRA contributions are subject to income limitations. Individuals exceeding these limits may be unable to contribute to a Roth IRA.

- Tax Implications: The tax implications of contributions and withdrawals differ between Traditional and Roth IRAs. It is crucial to understand these implications and choose the IRA type that aligns with individual circumstances.

- Investment Strategy: The choice of investments within an IRA is critical for long-term growth. Individuals should consider their risk tolerance, investment goals, and time horizon when making investment decisions.

- Retirement Planning: Catch-up contributions should be considered as part of a comprehensive retirement plan, factoring in other sources of income and expenses.

Frequently Asked Questions (FAQs) Regarding IRA Contribution Limits for Individuals Over 50

Q: What is the difference between a Traditional IRA and a Roth IRA?

A: Traditional IRAs allow individuals to deduct contributions from their taxable income, reducing their current tax liability. However, withdrawals in retirement are taxed. Roth IRAs, on the other hand, do not offer tax deductions for contributions but provide tax-free withdrawals in retirement.

Q: Can I contribute to both a Traditional and Roth IRA in the same year?

A: Yes, individuals can contribute to both a Traditional and Roth IRA in the same year, provided they do not exceed the annual contribution limit for each account type.

Q: Can I contribute to a 401(k) and an IRA in the same year?

A: Yes, individuals can contribute to both a 401(k) and an IRA in the same year, but the total contribution amount cannot exceed the annual contribution limit for each account type.

Q: What happens if I exceed the contribution limit?

A: Exceeding the contribution limit can result in penalties and taxes. It is crucial to stay within the allowed limits to avoid these consequences.

Q: What are the income limits for Roth IRA contributions?

A: For 2023, the income limits for Roth IRA contributions are $153,000 for single filers and $228,000 for married couples filing jointly. These limits may adjust slightly for 2025.

Tips for Maximizing IRA Contributions for Individuals Over 50

- Start Early: The earlier individuals begin saving, the more time their investments have to grow.

- Automate Contributions: Setting up automatic contributions from a checking account can help ensure consistent saving.

- Consider Catch-Up Contributions: Don’t overlook the opportunity to maximize retirement savings through catch-up contributions.

- Seek Professional Advice: Consult with a financial advisor to develop a personalized retirement plan that aligns with individual goals and circumstances.

Conclusion

IRA contribution limits for individuals over 50 offer a valuable opportunity to accelerate retirement savings and enhance financial security. By understanding the rules, benefits, and implications associated with catch-up contributions, individuals can make informed decisions to maximize their retirement savings potential. Staying informed about upcoming changes in contribution limits and seeking professional advice are crucial steps in navigating the complexities of retirement planning. By taking advantage of these resources and making informed choices, individuals can confidently work towards a comfortable and financially secure retirement.

Closure

Thus, we hope this article has provided valuable insights into Navigating Retirement Savings in 2025: Understanding the IRA Contribution Limits for Individuals Over 50. We appreciate your attention to our article. See you in our next article!