Navigating Retirement Savings: Understanding Roth IRA Contribution Limits for Individuals Over 65 in 2025

Navigating Retirement Savings: Understanding Roth IRA Contribution Limits for Individuals Over 65 in 2025

Introduction

In this auspicious occasion, we are delighted to delve into the intriguing topic related to Navigating Retirement Savings: Understanding Roth IRA Contribution Limits for Individuals Over 65 in 2025. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating Retirement Savings: Understanding Roth IRA Contribution Limits for Individuals Over 65 in 2025

The Roth IRA, a popular retirement savings tool, offers tax-free withdrawals in retirement. While many associate Roth IRAs with younger savers, individuals over 65 also benefit from their potential to grow wealth tax-free. This article delves into the contribution limits for Roth IRAs in 2025, specifically for those aged 65 and older, providing a comprehensive understanding of this valuable retirement savings option.

Understanding the Roth IRA Contribution Limits

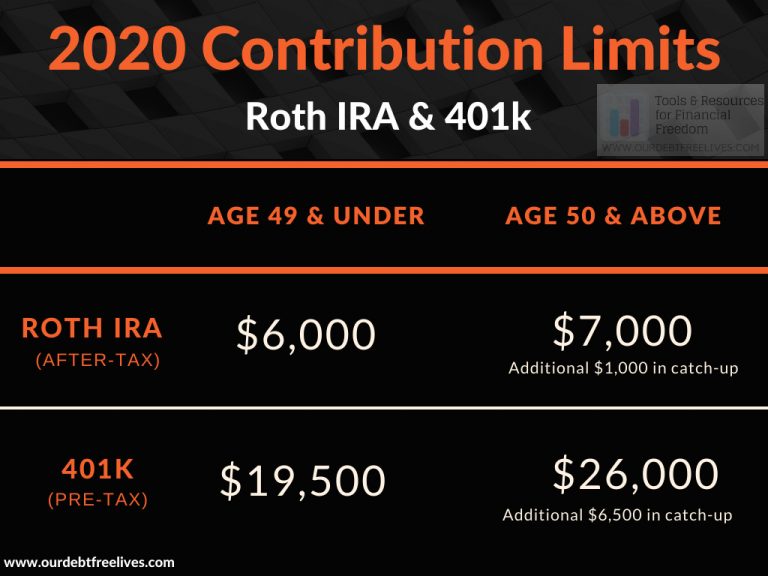

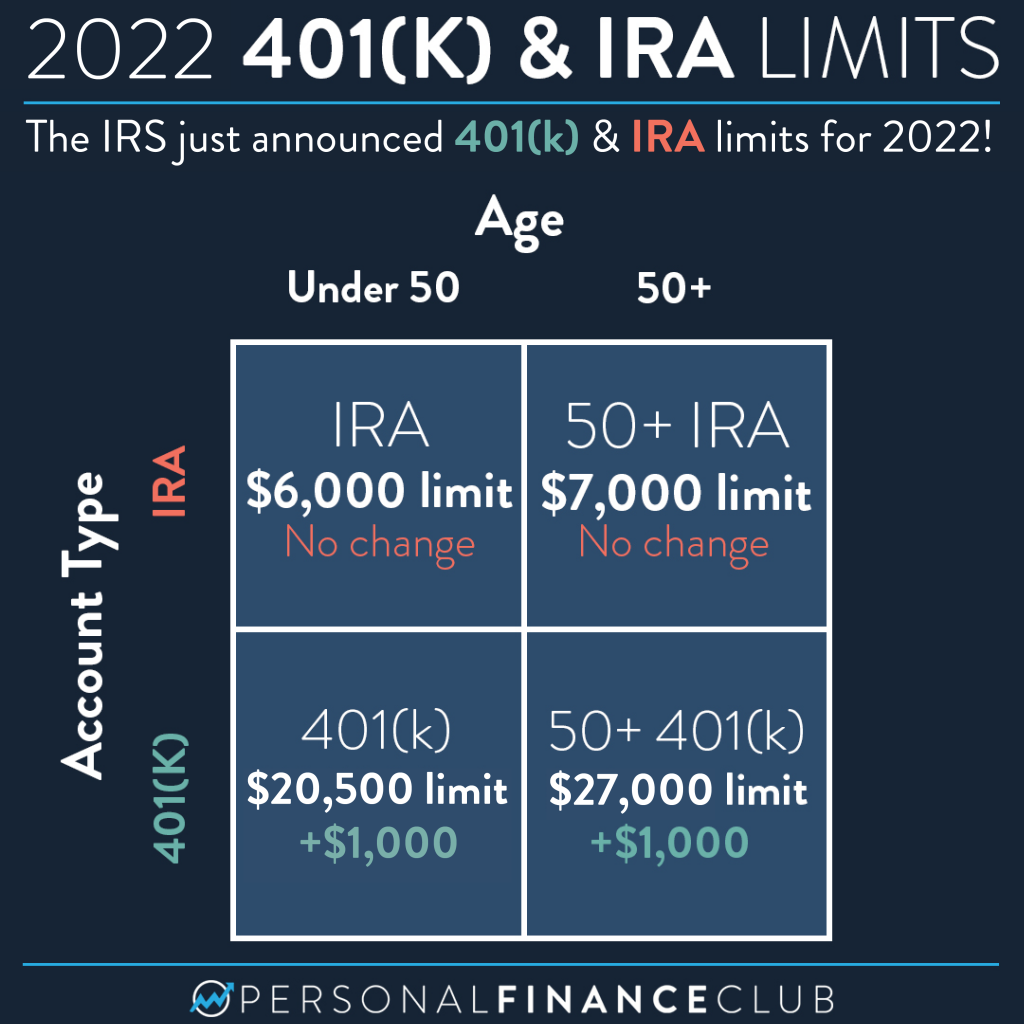

The annual contribution limit for Roth IRAs in 2025 is expected to remain at $6,500. However, individuals aged 50 and older are eligible for an additional "catch-up" contribution, which for 2025 is projected to be $1,000. This means that those over 65 can contribute a total of $7,500 to their Roth IRA in 2025.

Key Considerations for Individuals Over 65

While the contribution limit for Roth IRAs remains consistent regardless of age, several factors come into play for individuals over 65:

- Modified Adjusted Gross Income (MAGI): Eligibility for Roth IRA contributions depends on your Modified Adjusted Gross Income (MAGI). In 2025, if your MAGI exceeds a certain threshold, you may not be able to contribute to a Roth IRA. The exact income limits for 2025 are not yet finalized.

- Required Minimum Distributions (RMDs): Individuals with traditional IRAs or 401(k)s are generally required to start taking Required Minimum Distributions (RMDs) from their accounts beginning at age 73. These RMDs are taxable. If you are over 65 and have already started taking RMDs, you may find Roth IRA contributions more appealing as they offer tax-free withdrawals in retirement.

- Tax Implications: While Roth IRA contributions are made with after-tax dollars, withdrawals in retirement are tax-free. This can be particularly beneficial for individuals in higher tax brackets, as it allows them to avoid paying taxes on their retirement income.

Benefits of Roth IRAs for Individuals Over 65

- Tax-Free Growth: The primary advantage of Roth IRAs is the tax-free growth of your investments. As your contributions and earnings accumulate, they grow tax-deferred, and withdrawals in retirement are tax-free.

- Flexibility: Roth IRAs offer greater flexibility compared to traditional IRAs. You can withdraw contributions at any time without penalty, making them a valuable resource for unexpected expenses.

- Potential for Estate Planning: Roth IRAs can be a powerful tool for estate planning. Your beneficiaries can inherit your Roth IRA and receive tax-free distributions.

FAQs about Roth IRA Contribution Limits for Individuals Over 65

Q: If I am over 65 and my MAGI exceeds the limit for Roth IRA contributions, can I still contribute to a traditional IRA?

A: Yes, you can still contribute to a traditional IRA, regardless of your MAGI. However, withdrawals from a traditional IRA are generally taxable in retirement.

Q: If I am over 65 and have already started taking RMDs, can I still contribute to a Roth IRA?

A: Yes, you can still contribute to a Roth IRA, even if you are taking RMDs from other retirement accounts.

Q: Can I contribute to both a Roth IRA and a traditional IRA in the same year?

A: Yes, you can contribute to both a Roth IRA and a traditional IRA in the same year, as long as you do not exceed the total annual contribution limits for each type of account.

Q: If I contribute to a Roth IRA after age 70 1/2, will I be required to take RMDs from the account?

A: No, Roth IRAs are not subject to RMDs, even after age 70 1/2.

Tips for Maximizing Your Roth IRA Contributions

- Consider your financial situation: Before contributing to a Roth IRA, assess your income and expenses. Make sure you can afford the contributions without jeopardizing your other financial goals.

- Contribute early and often: The earlier you start contributing, the more time your investments have to grow tax-free.

- Diversify your investments: Spread your contributions across different asset classes, such as stocks, bonds, and real estate, to reduce risk and maximize potential returns.

- Seek professional advice: Consult with a financial advisor to determine if a Roth IRA is the right choice for your specific circumstances.

Conclusion

Understanding the contribution limits and benefits of Roth IRAs is crucial for individuals over 65 planning for a comfortable retirement. While the contribution limit for Roth IRAs remains consistent, the tax implications and eligibility requirements can change depending on your individual circumstances. By carefully considering your options and seeking professional guidance, you can effectively utilize Roth IRAs to build a secure financial future.

/tradition-ira-roth-ira-contribution-limits-5a01592613f1290037067ebc.jpg)

Closure

Thus, we hope this article has provided valuable insights into Navigating Retirement Savings: Understanding Roth IRA Contribution Limits for Individuals Over 65 in 2025. We appreciate your attention to our article. See you in our next article!