Navigating Retirement Savings: Understanding the 2025 Simple IRA Contribution Limits for Individuals Over 50

Navigating Retirement Savings: Understanding the 2025 Simple IRA Contribution Limits for Individuals Over 50

Introduction

In this auspicious occasion, we are delighted to delve into the intriguing topic related to Navigating Retirement Savings: Understanding the 2025 Simple IRA Contribution Limits for Individuals Over 50. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating Retirement Savings: Understanding the 2025 Simple IRA Contribution Limits for Individuals Over 50

Retirement planning is a critical aspect of financial well-being, and maximizing contributions to retirement accounts is essential for securing a comfortable future. The Simple IRA, a retirement savings plan designed for small businesses and self-employed individuals, offers a valuable opportunity to accumulate wealth for retirement. For individuals over 50, the Simple IRA provides an additional advantage – the ability to contribute a larger amount, known as the "catch-up" contribution.

This article aims to clarify the contribution limits for Simple IRAs in 2025, specifically for those aged 50 and above. It will delve into the benefits of this catch-up contribution, explore strategies for maximizing retirement savings, and address frequently asked questions about this aspect of retirement planning.

The 2025 Simple IRA Contribution Limits: A Breakdown

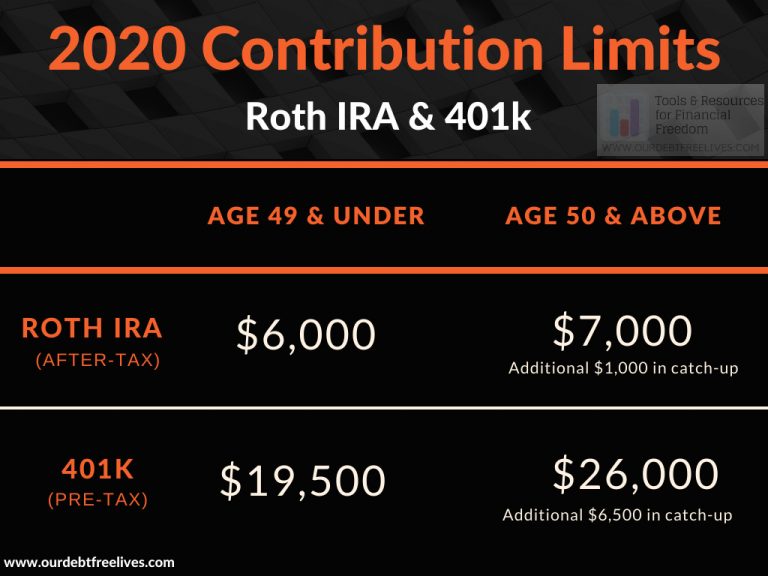

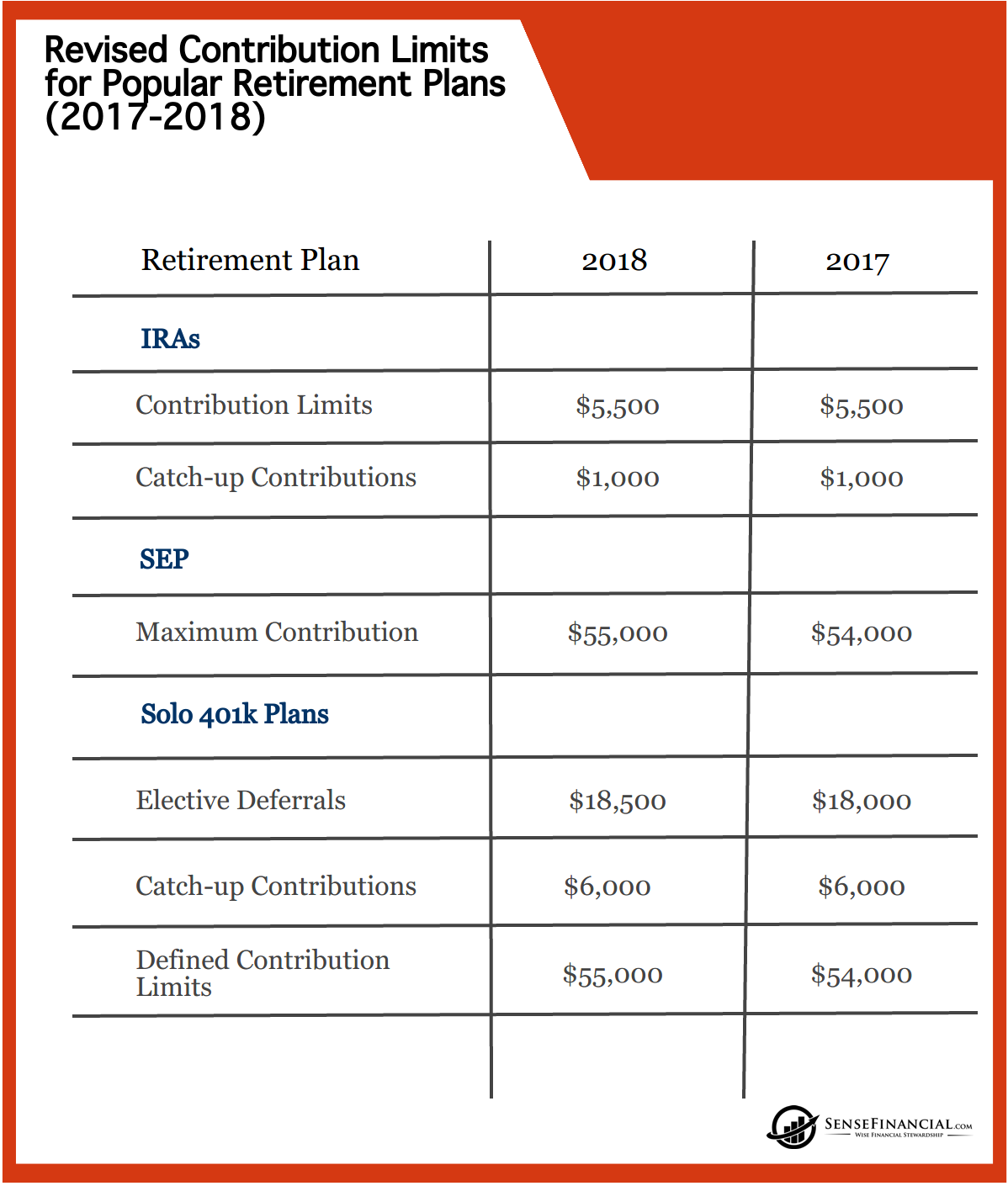

The IRS sets annual contribution limits for Simple IRAs, which are subject to change. For 2025, the maximum contribution limit for individuals under 50 is expected to remain at $15,500. However, individuals aged 50 and older can contribute an additional $3,500 in 2025, bringing their total contribution limit to $19,000.

This catch-up contribution serves as a valuable tool for those approaching retirement, allowing them to bridge the gap between their current savings and their desired retirement income. The extra contribution can significantly bolster retirement funds, potentially making a significant difference in the long run.

Understanding the Benefits of the Catch-Up Contribution

The catch-up contribution offers several advantages for individuals over 50:

- Accelerated Savings: The extra contribution allows individuals to save more aggressively in the years leading up to retirement, potentially accelerating their path to financial independence.

- Tax Advantages: Contributions to a Simple IRA are made pre-tax, meaning they reduce taxable income in the year they are made. This can lead to immediate tax savings, making retirement planning more affordable.

- Compounding Growth: The power of compounding works in favor of those who contribute more. By maximizing contributions, individuals can benefit from greater long-term growth, potentially leading to a larger nest egg in retirement.

- Increased Flexibility: The catch-up contribution provides flexibility for individuals who may have fallen behind on their retirement savings or want to ensure they have enough to cover their needs in retirement.

Maximizing Your Contributions: Strategies for Success

To make the most of the 2025 Simple IRA contribution limits, consider these strategies:

- Contribute the Maximum: Maximize your contributions each year to take full advantage of the tax benefits and accelerate your savings growth.

- Automate Contributions: Set up automatic contributions from your paycheck to your Simple IRA. This ensures consistent savings and eliminates the need for manual adjustments.

- Review Your Contribution Level Regularly: As your income increases, consider increasing your contribution amount to maintain your savings trajectory.

- Seek Professional Advice: Consult with a financial advisor to create a personalized retirement plan that considers your specific financial goals and risk tolerance.

Frequently Asked Questions (FAQs) about 2025 Simple IRA Contribution Limits

Q: Who is eligible for a Simple IRA?

A: Simple IRAs are available to small businesses and self-employed individuals with 100 or fewer employees.

Q: Can I contribute to both a Simple IRA and a Traditional IRA?

A: No, you cannot contribute to both a Simple IRA and a Traditional IRA simultaneously.

Q: What happens to my Simple IRA contributions when I retire?

A: Once you retire, you can begin withdrawing funds from your Simple IRA. Withdrawals before age 59 1/2 are generally subject to a 10% early withdrawal penalty, unless you qualify for an exception.

Q: Are there any income limits for contributing to a Simple IRA?

A: There are no income limits for contributing to a Simple IRA.

Q: Can I change my contribution amount during the year?

A: Yes, you can change your contribution amount during the year. However, it’s important to consult with your employer or administrator to ensure you are following the correct procedures.

Tips for Maximizing Your Simple IRA Contributions

- Start Early: The earlier you begin saving for retirement, the greater the potential for growth due to compounding.

- Invest Wisely: Choose investment options that align with your risk tolerance and long-term financial goals.

- Diversify Your Investments: Spread your investments across different asset classes, such as stocks, bonds, and real estate, to mitigate risk.

- Stay Informed: Stay updated on changes in contribution limits and other relevant retirement planning regulations.

Conclusion: Securing Your Future with the Simple IRA Catch-Up Contribution

The Simple IRA, with its catch-up contribution option for individuals over 50, provides a powerful tool for building a secure retirement. By maximizing contributions and implementing strategic savings strategies, individuals can accelerate their path to financial independence and ensure a comfortable future. Understanding the intricacies of these contribution limits and taking advantage of the benefits they offer is crucial for achieving long-term financial well-being. Remember, the power to shape your retirement lies in your hands, and maximizing your contributions is a significant step towards achieving your financial goals.

Closure

Thus, we hope this article has provided valuable insights into Navigating Retirement Savings: Understanding the 2025 Simple IRA Contribution Limits for Individuals Over 50. We thank you for taking the time to read this article. See you in our next article!