Navigating the 2025 Roth IRA Contribution Limits for Individuals Aged 50 and Over

Navigating the 2025 Roth IRA Contribution Limits for Individuals Aged 50 and Over

Introduction

With great pleasure, we will explore the intriguing topic related to Navigating the 2025 Roth IRA Contribution Limits for Individuals Aged 50 and Over. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating the 2025 Roth IRA Contribution Limits for Individuals Aged 50 and Over

The Roth IRA, a popular retirement savings vehicle, offers tax-free withdrawals in retirement, making it a valuable tool for individuals seeking to secure their financial future. For individuals aged 50 and over, the Roth IRA presents a unique opportunity to contribute an additional amount, known as the "catch-up contribution," to their retirement savings. Understanding these contribution limits and their implications is crucial for maximizing retirement savings potential.

The 2025 Contribution Limits

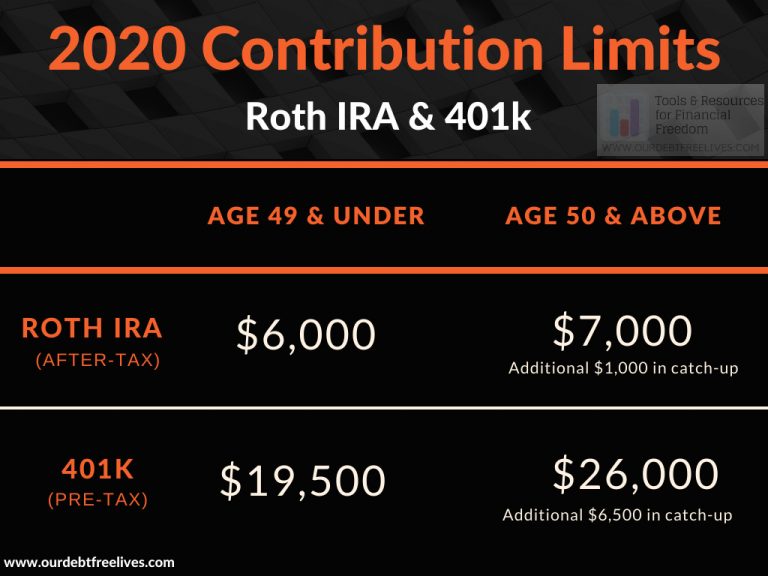

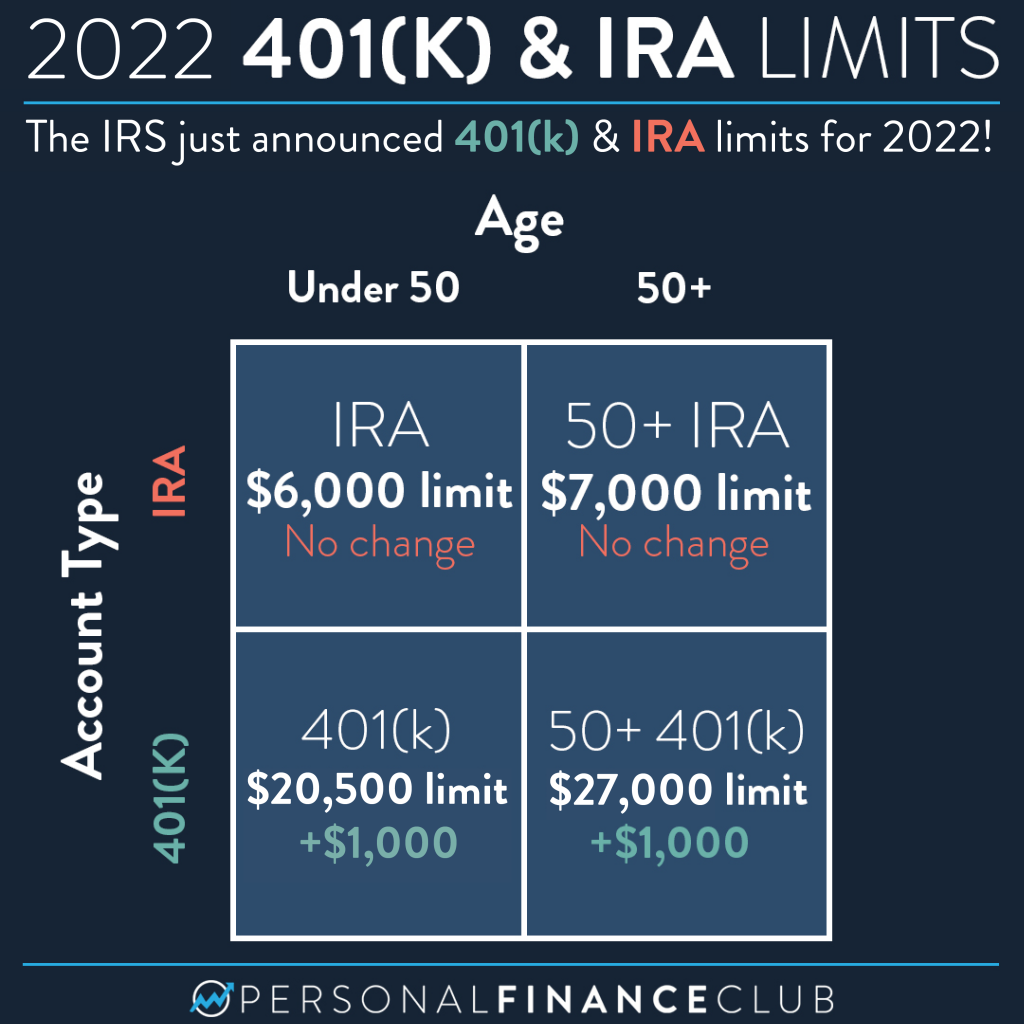

The Internal Revenue Service (IRS) sets annual contribution limits for Roth IRAs, which are subject to change. As of 2023, the annual contribution limit for individuals of all ages is $6,500. However, individuals aged 50 and over can contribute an additional $1,000 per year, bringing their total contribution limit to $7,500. These limits are expected to increase slightly in 2025, reflecting adjustments for inflation.

The Value of Catch-Up Contributions

The catch-up contribution provides a significant opportunity for individuals aged 50 and over to accelerate their retirement savings. By contributing an extra $1,000 annually, individuals can significantly boost their retirement nest egg. This additional contribution can compound over time, yielding substantial returns in the long run.

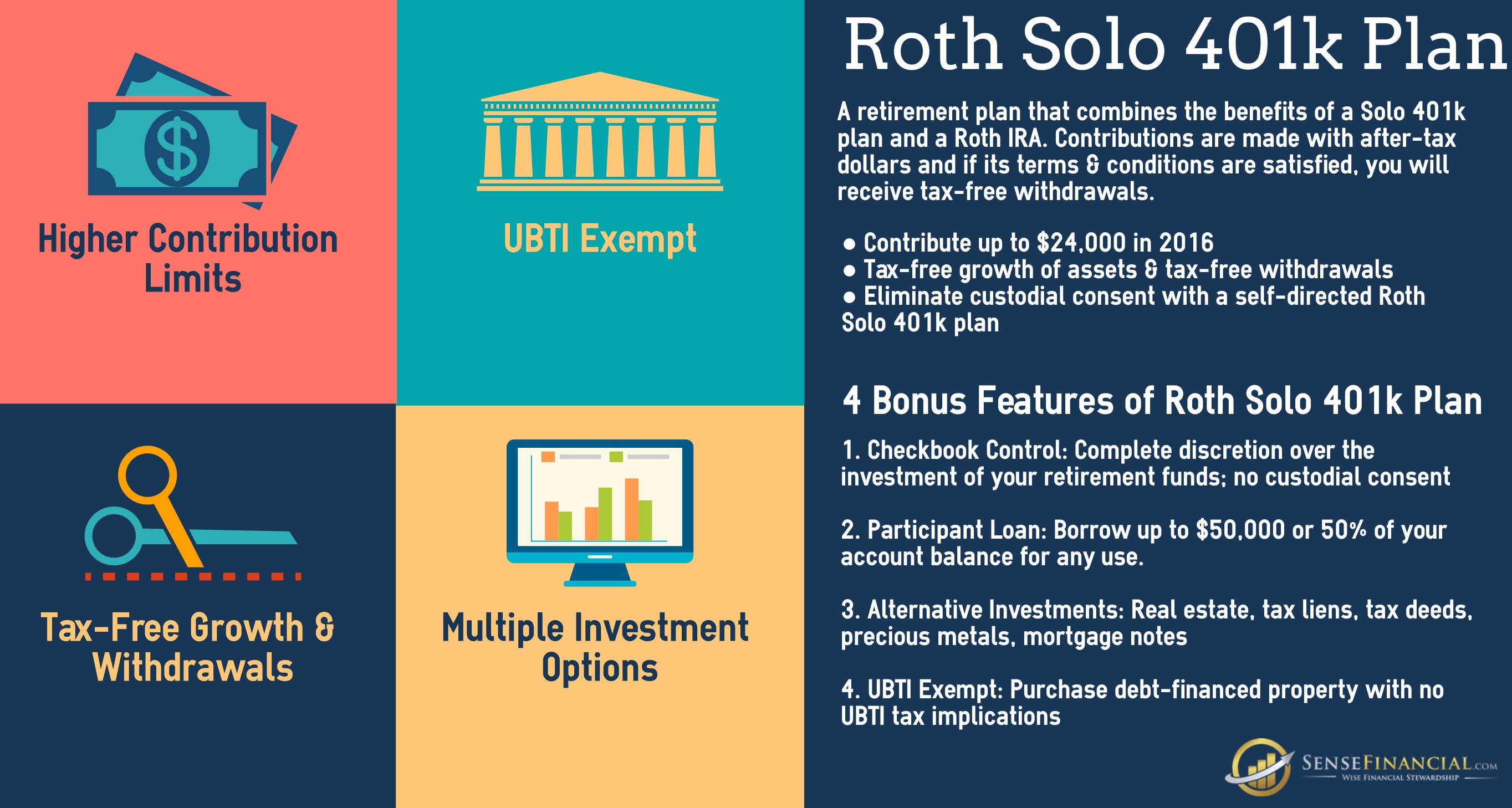

The Benefits of a Roth IRA

The Roth IRA offers numerous benefits for individuals looking to plan for their retirement, including:

- Tax-free withdrawals in retirement: Unlike traditional IRAs, where withdrawals are taxed in retirement, Roth IRA withdrawals are tax-free, allowing individuals to enjoy their retirement savings without any tax burden.

- Potential for tax-free growth: Earnings on contributions grow tax-deferred within the Roth IRA, offering the potential for tax-free compounding.

- Flexibility for early withdrawals: While generally discouraged, Roth IRA withdrawals are tax-free and penalty-free for qualified expenses, such as first-time home purchases, education costs, and certain medical expenses.

- Potential for estate planning: Roth IRAs can be passed on to beneficiaries tax-free, making them a valuable tool for estate planning.

Eligibility for Roth IRA Contributions

Individuals who meet the following criteria are eligible to contribute to a Roth IRA:

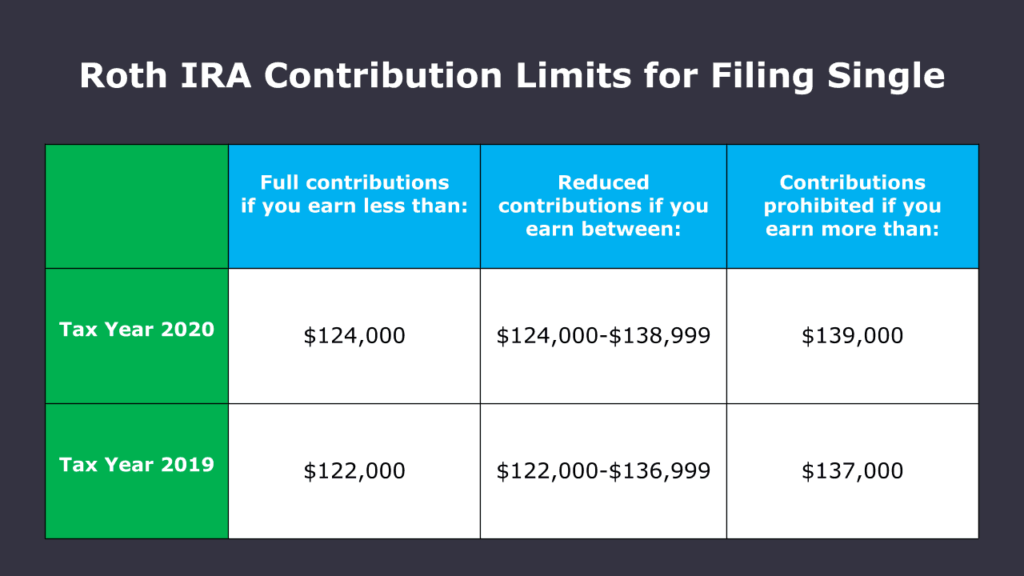

- Modified Adjusted Gross Income (MAGI) limits: The IRS sets MAGI limits for Roth IRA contributions. These limits vary based on filing status and are adjusted annually for inflation. For 2023, individuals filing as single or head of household can contribute to a Roth IRA if their MAGI is $153,000 or less. For married couples filing jointly, the MAGI limit is $228,000.

- Age: There is no age limit for contributing to a Roth IRA. However, individuals aged 50 and over are eligible for the additional catch-up contribution.

Important Considerations

While the Roth IRA offers substantial benefits, it is crucial to consider the following factors:

- Tax implications: Although withdrawals are tax-free in retirement, contributions are made with after-tax dollars. Individuals should consider their current tax bracket and future tax projections when deciding between a Roth IRA and a traditional IRA.

- Income limitations: As mentioned earlier, income limits apply to Roth IRA contributions. Individuals exceeding these limits may not be eligible to contribute to a Roth IRA.

- Investment options: Roth IRAs offer a wide range of investment options, allowing individuals to tailor their portfolio to their risk tolerance and investment goals. It is important to carefully select investments that align with these factors.

FAQs

1. Can I contribute to a Roth IRA if I already have a 401(k)?

Yes, you can contribute to both a Roth IRA and a 401(k) simultaneously. However, you may need to consider your income limits for each account.

2. Can I contribute to a Roth IRA if I am already retired?

Yes, you can continue contributing to a Roth IRA even after retirement, as long as you meet the eligibility requirements.

3. What happens to my Roth IRA contributions if I pass away?

Your Roth IRA will be passed on to your beneficiaries, who can then withdraw the funds tax-free.

4. Can I withdraw my Roth IRA contributions before retirement?

Yes, you can withdraw your contributions from a Roth IRA at any time without penalty. However, earnings may be subject to taxes and penalties if withdrawn before age 59 1/2.

5. What happens if I exceed the Roth IRA contribution limits?

The IRS imposes penalties for exceeding contribution limits. It is crucial to stay within the prescribed limits to avoid any penalties.

Tips for Maximizing Roth IRA Contributions

- Contribute the maximum amount possible: Maximize your contributions to take full advantage of the tax benefits and compound growth potential.

- Consider the catch-up contribution: If you are aged 50 or over, utilize the catch-up contribution to accelerate your retirement savings.

- Invest wisely: Choose investments that align with your risk tolerance, time horizon, and investment goals.

- Review your portfolio regularly: Monitor your investments and adjust your portfolio as needed to meet your changing needs and market conditions.

Conclusion

The 2025 Roth IRA contribution limits, particularly the catch-up contribution for individuals aged 50 and over, provide a valuable opportunity to boost retirement savings. By understanding the eligibility requirements, benefits, and potential drawbacks, individuals can make informed decisions about their retirement planning. Careful planning and strategic contributions can help individuals secure a comfortable and financially secure retirement.

Closure

Thus, we hope this article has provided valuable insights into Navigating the 2025 Roth IRA Contribution Limits for Individuals Aged 50 and Over. We hope you find this article informative and beneficial. See you in our next article!